It's a great time to borrow, fantastic, probably one of the best. Interest rates are low, and inflation seems to loom. Borrow money now at a cheap rate and pay it back with dollars worth less in the future. No question it's a great borrowing opportunity.

The tough part is what to buy. San Francisco housing could probably give up 10% or more (I have no idea, I don't live there are watch it, I'm mostly basing that on what I know has been a long run-up). My house in LA dropped $200k from where I bought it during the last bubble. I don't think that we're headed for another 2008 in housing. That situation was insane. People were forging mortgage applications left and right, they were buying places with 5 year ARM mortgages with zero down (or negative interest), and expected to make hundreds of thousands of equity in a few short years and do it again. Some people did, and laddered through 6 or 7 properties, and they were crapping their pants when the rates jumped, prices dropped, and their ARMs broke loose.

That kind of insanity is not what I see right now. I see a lot of people who are wary of housing. And that makes me think there is no way it could be as bad as it was. The behavior I saw in 2007 and the years leading up to it was bonkers, there-is-no-way-this-is-real, something-has-to-give, how can this be happening type behavior. Today seems absolutely tame by comparison, and people have fresh memories of that time keeping them from over-doing it.

I think we could see a drop in housing prices, but I seriously doubt that it goes south hard like it did. But what do I know? I lost $200k in real estate once already.

For a recession, optimally you have cash and area ready to buy when the stock market drops. But for right now, with inflation looming, I'm not sure cash is a great idea. This is a tighter spot than recessions might normally be.

Based on my obversvations of home price history on Zillow (not comprehensive, of course) it appears that many homes in the Bay Area peaked around 2007 and then dropped like a good 35-60% (!!) during the recession. They peaked again towards the middle of 2018 at around 10% higher than the pre-recession peaks (call it a 100% or more increase over recession lows) and have tapered or dropped slightly since then. If the pre-recession prices are understood to be caused by a speculative bubble, and the economic landscape of the Bay Area hasn't changed drastically (tech and high-pay was here before, during, and after the Financial Crisis) and population growth has only been about 3%....it seems to me prices are too high. Probably not 50% too high, but I don't think 25% is too much of an overestimate,

for the Bay Area.

Note: I think foreign investment (there are

a lot of empty condos around), investors buying up supply during the recession for rentals, and short-term rental conversions have really cut into the supply. The lack of buildable land, the fierce opposition to development (NIMBY), absurd labor rates ('shop electricians charge $75/hr!!!) and extensive entitlements processes have also hurt the ability of the system to provide adequate supply. Basically there is a long host of issues why Bay Area housing prices are through the roof, and I think it's compounded by a fair amount of speculation.

Hope #1 is that a lot of folks that have been here a long time and are property owners, are seeing a recession on the Horizon and see a closing window for them to cash out on their properties to fund their retirement. Marin county, especially has a very high proportion of seniors (25% of residents are 65+) and they all own property. The big issue with that theory is that Marin county is pretty much already an ideal retirement location (near-perfect weather, good communities, great landscape, outdoor activities, etc) and seniors who own already probably can do so at relatively little expensive because they likely bought years, if not decades ago.

Hope #2 is that existing investment property owners (institutional or otherwise) are going to be fearful of missing the opportunity to cash in those 100%+ returns they achieved when they bought during the recession and will do whatever they can to sell before a housing market downturn materializes. If enough of them do that simultaneously, it will suppress prices to a more reasonable level.

So my plan is to just save and diversify as much as I can now so that I can be well positioned to mobilize in the event of a downturn. The last thing I want to do is buy now (relenting to fear that prices will keep going up) and then watch my equity tank in 2-3 years while possibly also losing my job. The risk, of course, is that prices

do keep going up (I don't honestly think they can go much higher, a 500SF condo costs $500k in so-so locations, for God's sake) and well and truly miss my chance. In that case, I will likely leave SF - this damn pressure cooker. So pretty though.

I wish I had been cognisant of what was happening during the 04-07 housing boom. I mean I was like 15 years old, so I'll give myself a pass, but I'd like to think I would have seen the bust coming if I was my current age back then. Imagine going in in 2010 and buying up all these 500-1000sf condos in San Francisco for like $150-200k. You could have made an absolute killing either as rentals or as longer-term holdings.

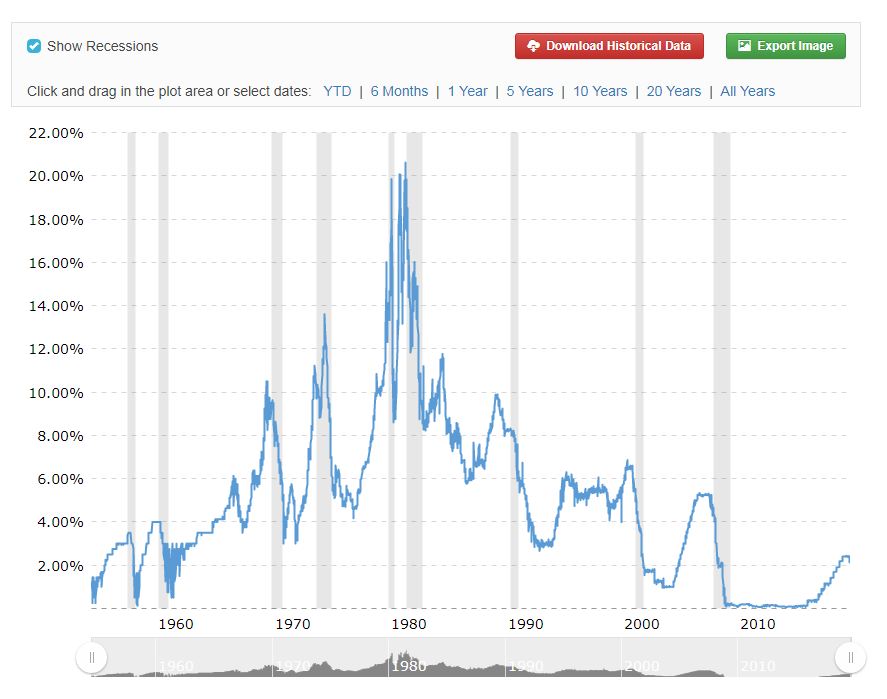

Do you think we are headed to a period of 1970s-style stagflation? That would be a real big bummer. The government has so much debt...they're gonna have to print money to pay it off or raise taxes...not something i would expect most presidents to do, let alone Trump. If they do that during a recession...**** that is gonna suck.