- 11,292

- Marin County

There doesn't appear to be any sort of general economy thread here (well, one from 2003...), so I thought I'd start one.

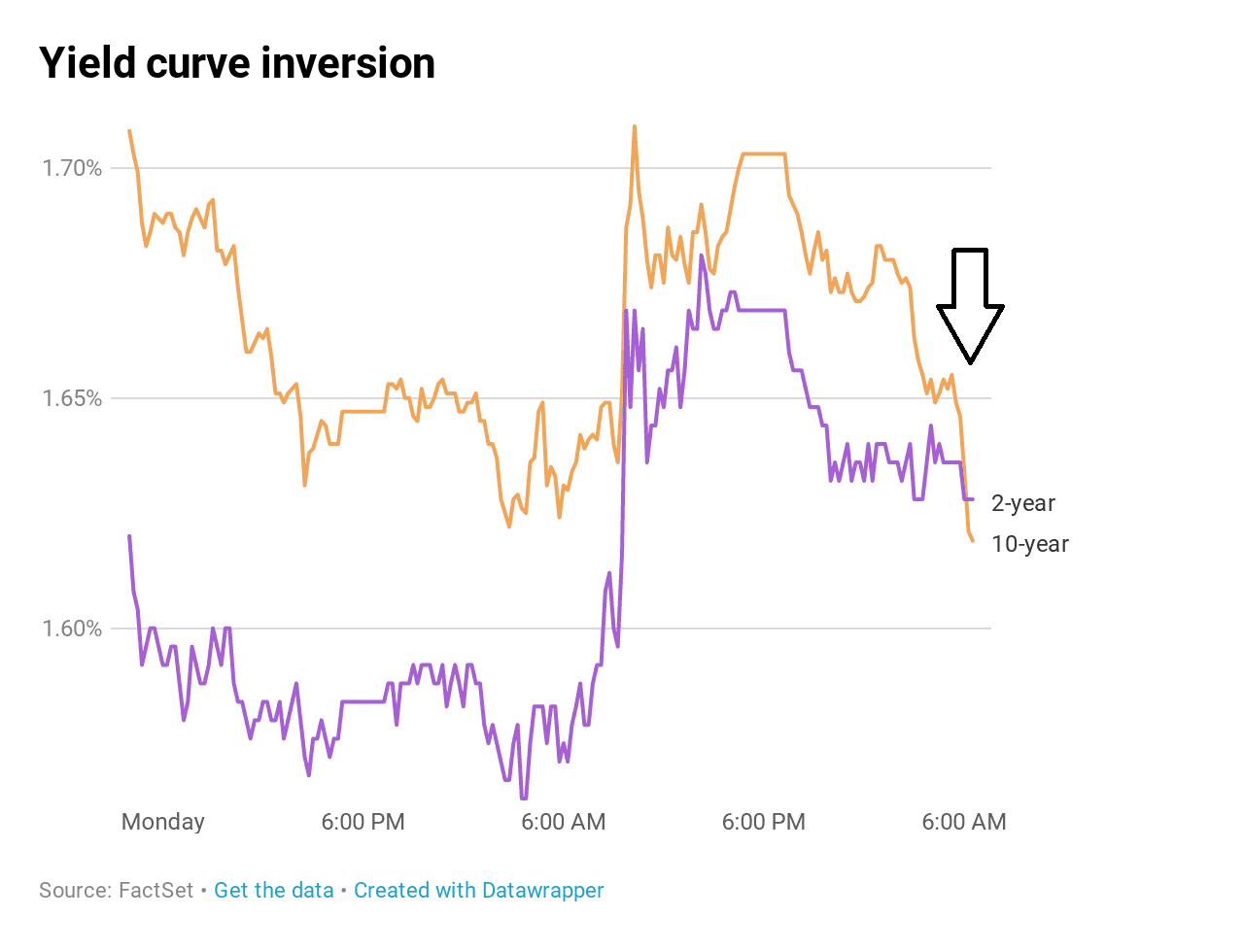

I think the most interesting thing happening right now is the $15T worth of negative yielding sovereign bonds being traded around. How is this going to impact fixed income funds in the years to come? What would an overvalued bond market collapse even look like?

edit: I should note that some sovereign bond yields are at unprecedentedly low yields. Like lowest yields in 250+ years unprecedented. Like genuine "we've never seen this" territory.

Some other thoughts:

How much is automated/algorithmic trading keeping the bottom from falling out of the stock market and how long can this artificial prop (if that's whats happening) keep it from doing so? As in, is there a algorithmic trading "bubble"?

How can we make building housing (quickly becoming a huge problem all around the country, especially in dense areas) more attractive to builders? Or how can we building more housing using alternative methods?

The "trade war" is obviously a big economic headline, but I find it boring.

I think the most interesting thing happening right now is the $15T worth of negative yielding sovereign bonds being traded around. How is this going to impact fixed income funds in the years to come? What would an overvalued bond market collapse even look like?

edit: I should note that some sovereign bond yields are at unprecedentedly low yields. Like lowest yields in 250+ years unprecedented. Like genuine "we've never seen this" territory.

Some other thoughts:

How much is automated/algorithmic trading keeping the bottom from falling out of the stock market and how long can this artificial prop (if that's whats happening) keep it from doing so? As in, is there a algorithmic trading "bubble"?

How can we make building housing (quickly becoming a huge problem all around the country, especially in dense areas) more attractive to builders? Or how can we building more housing using alternative methods?

The "trade war" is obviously a big economic headline, but I find it boring.

Last edited: